Wenting MaThis email address is being protected from spambots. You need JavaScript enabled to view it.

School of Finance and Economic, Zhengzhou University of Science and Technology, Zhengzhou, Henan, China 450064

Received: March 14, 2025 Accepted: April 5, 2025 Publication Date: May 1, 2025

Copyright The Author(s). This is an open access article distributed under the terms of the Creative Commons Attribution License (CC BY 4.0), which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are cited.

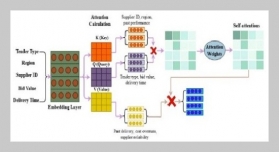

Financial risk prediction for enterprises is a hot topic in the field of financial technology. Deep learning-Based methods achieve encouraging the financial risk prediction performance due to the power ability of the feature learning. However, there exists two issues in deep learning-Based methods. (1) Current methods fail to accurately model the complex relationships among listed companies in the real financial market. (2) Current methods lack credible estimates in the decision-making process, which leads to the questionable reliability of the decision-making results. To this end, a trustworthy-constraint deep graph learning network (TDGL-net) is proposed to achieve the above goal, which includes the multi-view feature encoding, the heterogeneous graph information aggregation, the trustworthy decision-making mechanism. Specifically, TDGL-net integrates a multi-dimensional bilinear neural tensor and Transformer into a unified multi-view feature encoding to learn comprehensive representation. Then, TDGL-net models heterogeneous graph information aggregation via the cross-category association and the intra-category association, to capture complex inter-enterprise relationships with momentum spillover effects for enhancing the representation discrimination. Additionally, TDGL-net incorporates a trustworthy decision-making mechanism to adaptively integrate information from deep embedding representations and graph embedding representations according to enterprise-specific contexts, improving decision reliability and accuracy. Ultimately, extensive experimental evaluations on the real-world dataset reveal that TDGL-net delivers state-of-the-art performance in predicting enterprise financial risk.

[1] H.Xia, H. Ao, L. Li, Y. Liu, S. Liu, G. Ye, and H. Chai. “CI-STHPAN: pre-trained attention network for stock selection with channel-independent spatio-temporal hypergraph”. In: Proceedings of the AAAI Conference on Artificial Intelligence. 38. 8. 2024, 9187–9195. DOI: 10.1609/aaai.v38i8.28770.

[2] C. Xu, H. Huang, X. Ying, J. Gao, Z. Li, P. Zhang, J. Xiao, J. Zhang, andJ. Luo, (2022) “HGNN:Hierarchical graph neural network for predicting the classification of price-limit-hitting stocks" Information Sciences 607: 783–798. DOI: 10.1016/j.ins.2022.06.010.

[3] J. Gao, M. Liu, P. Li, J. Zhang, and Z. Chen, (2024) “Deep Multiview Adaptive Clustering With Semantic In variance" IEEE Transactions on Neural Networks and Learning Systems 35(9): 12965–12978. DOI: 10.1109/TNNLS.2023.3265699.

[4] M.Leippold, Q.Wang,andW.Zhou,(2022)“Machine learning in the Chinese stock market" Journal of Financial Economics 145(2): 64–82. DOI: 10.1016/j.jfineco.2021.08.017.

[5] P. Li, J. Gao, J. Zhang, S. Jin, and Z. Chen, (2022) “Deep Reinforcement Clustering" IEEE Transactions on Multimedia: DOI: 10.1109/TMM.2022.3233249.

[6] P. Li, Z. Chen, L. T. Yang, Q. Zhang, and M. J. Deen, (2017) “Deep convolutional computation model for feature learning on big data in internet of things" IEEE Transac tions on Industrial Informatics 14(2): 790–798. DOI: 10.1109/TII.2017.2739340.

[7] P. Li, A. A. Laghari, M. Rashid, J. Gao, T. R. Gadekallu, A. R. Javed, and S. Yin, (2022) “A deep multimodal adversarial cycle-consistent network for smart enterprise system" IEEE Transactions on Industrial Informatics 19(1): 693–702. DOI: 10.1109/TII.2022.3197201.

[8] W. Bao, Y. Cao, Y. Yang, H. Che, J. Huang, and S. Wen, (2024) “Data-driven stock forecasting models based on neural networks: A review" Information Fusion: 102616. DOI: 10.1016/j.inffus.2024.102616.

[9] R. Cheng and Q. Li. “Modeling the momentum spillover effect for stock prediction via attribute driven graph attention networks”. In: Proceedings of the AAAI conference on artificial intelligence. 35. 1. 2021, 55–62. DOI: 10.1609/aaai.v35i1.16077.

[10] K. Du, R. Mao, F. Xing, and E. Cambria. “A dynamic dual-graph neural network for stock price movement prediction”. In: 2024 International Joint Conference on Neural Networks (IJCNN). 2024, 1–8. DOI: 10.1109/ IJCNN60899.2024.10650440.

[11] T. N. Kipf and M. Welling, (2016) “Semi-supervised classification with graph convolutional networks" arXiv preprint arXiv:1609.02907:

[12] P.Velickovic, G. Cucurull, A. Casanova, A. Romero, P. Lio, Y. Bengio, et al., (2017) “Graph attention networks" stat 1050(20): 10–48550.

[13] Z.Hu, Y.Dong, K.Wang, and Y.Sun.“Heterogeneous graph transformer”. In: Proceedings of the web confer ence 2020. 2020, 2704–2710. DOI: 10.1145/3366423.338002.

[14] R. Sawhney, S. Agarwal, A. Wadhwa, and R. Shah. “Deep attentive learning for stock movement pre diction from social media text and company correlations”. In: Proceedings of the 2020 conference on empir ical methods in natural language processing (EMNLP). 2020, 8415–8426. DOI: 10.18653/v1/2020.emnlp-main.676.

[15] R. Sawhney, S. Agarwal, A. Wadhwa, T. Derr, and R. R. Shah. “Stock selection via spatiotemporal hy pergraph attention network: A learning to rank approach”. In: Proceedings of the AAAI Conference on Ar tificial Intelligence. 35. 1. 2021, 497–504. DOI: 10.1609/aaai.v35i1.16127.

[16] R. Cheng and Q. Li. “Modeling the momentum spillover effect for stock prediction via attribute driven graph attention networks”. In: Proceedings of the AAAI conference on artificial intelligence. 35. 1. 2021, 55–62. DOI: 10.1609/aaai.v35i1.16077.

We use cookies on this website to personalize content to improve your user experience and analyze our traffic. By using this site you agree to its use of cookies.